Property

Domestic Business

In 2018, the Korean property insurance market experienced a small increase in claims compared to the year before in the wake of several mid-sized typhoons, such as Kong-rey and Soulik in the third quarter, but the loss ratio remained relatively stable at 47.4 percent. In terms of premium growth, the market slightly rebounded from the downward trend that continued for several years, with premium income increasing by 2.7 percent to KRW 1,740 billion in 2018. This increase was backed by comprehensive insurance premiums, which grew by 4.7 percent to KRW 1,465 billion. On the other hand, fire insurance premiums declined by 7.2 percent to KRW 275 billion as rates continued to soften.

Adverse market conditions made 2018 a challenging year for Korean Re’s domestic property business, but we managed to bring negative impacts on our business to a limited level. We saw our domestic property premiums decrease by 3.9 percent to KRW 511 billion in 2018, as our fire insurance premiums shrank by 23.4 percent to KRW 113 billion amid an increase in retention by local primary insurers. It was encouraging, however, to see a 3.7 percent growth in our premium income from comprehensive insurance, which totaled KRW 398 billion. This was attributed to our ongoing efforts to develop new business. As we focused on selective underwriting, our business results for domestic property business remained stable.

As we enter 2019, we expect the domestic property insurance market to continue to suffer sluggish premium growth, with primary insurers increasing their retention levels. Despite the strain from this unfavorable market situation, we will keep rebalancing our domestic property business portfolio to maximize our profit potential. At the same time, we will maintain our underwriting strategy of exercising discipline based on exhaustive risk analysis so that we can increase profitable accounts, contributing to the company’s overall profitability.

Gross Written Premiums: Domestic Property Business

(Units: KRW billion, USD million)

|

FY 2018 |

FY 2018 |

FY 2017 |

FY 2017 |

|

|

Fire |

113.3 |

102.0 |

147.9 |

130.5 |

|

Comprehensive |

398.1 |

358.2 |

384.0 |

338.9 |

|

Total |

511.4 |

460.2 |

531.9 |

469.4 |

International Facultative Business

Our international property facultative business saw another year of strong growth, with gross written premiums soaring by 28.1 percent to KRW 104.3 billion in 2018. This resulted primarily from our efforts to increase line size on quality risks and to expand the current portfolio by exploring growth opportunities in untapped markets.

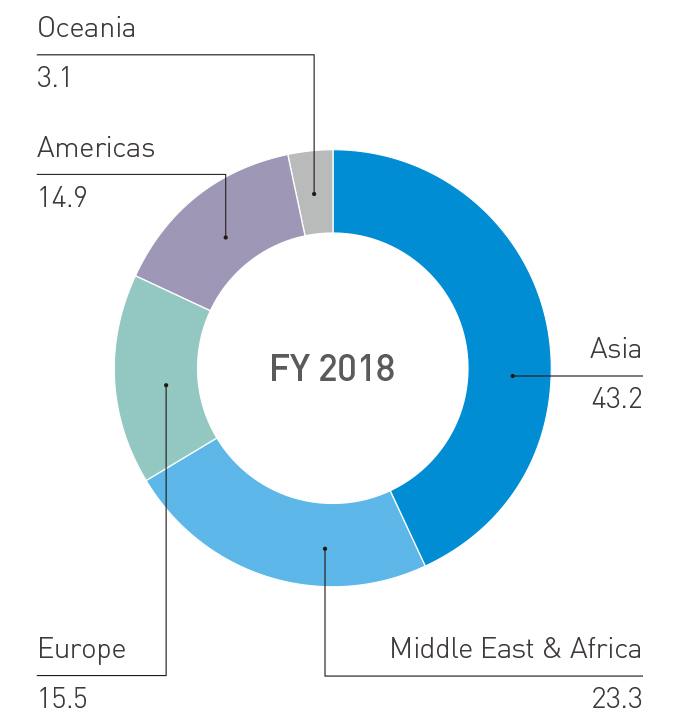

A breakdown of our premium income by geography shows that Asia is still our dominant market, comprising 43.2 percent of the total international property facultative business, followed by the Middle East and Africa (23.3 percent), Europe (15.5 percent), and the Americas (14.9 percent). The overall composition has not changed much from the prior year.

In 2018, we continued to implement our client support program with the aim of becoming a great business partner to our clients. For example, we hosted a Technical Engineering Seminar for our key clients in Malaysia and Thailand to help them find risk management solutions that meet their needs. It also served as an opportunity for us to share our underwriting techniques with regard to power and petrochemical occupancies. We will seek to have more of our key clients be involved in this engagement by expanding our client support service to other regions.

Following a series of large natural catastrophes in 2017, we have revised our underwriting guideline to limit our exposure in primary and low layers for risks located in catastrophe-prone areas. We have also focused on enhancing profitability by increasing our participation in proportional reinsurance business with strong risk management and healthy loss records. Meanwhile, our strategic initiative to expand into untapped markets has contributed much to the increase in our gross premiums, and we will make sure that this expansion is accompanied with exhaustive assessment as to whether those new markets are worth tapping into.

A protracted soft pricing cycle, heightened competition, and the risk of large catastrophe losses may continue to pose a challenge to our business profitability. However, there are signs of improvement in terms and rates, particularly in the area of power generation and downstream energy. When this positive change gathers pace, a more favorable pricing environment can be made sooner than expected. Moreover, we are hopeful that our strong credit ratings and ample capacity will be instrumental in helping our business partners fulfill their needs. Based on these strengths, we will endeavor to expand our presence both in the existing and new markets.

Gross Written Premiums: International Facultative Business

(Units: KRW billion, USD million)

|

FY 2018 |

FY 2018 |

FY 2017 |

FY 2017 |

|

|

International Facultative Business |

104.3 |

93.9 |

81.4 |

71.8 |

International Facultative Portfolio by Geography for 2018

(Unit: %)

International Treaty Business

In 2018, natural catastrophe insured losses worldwide were less than what was recorded in the previous year, but still reached as high as USD 90 billion. It was the fourth-costliest year ever behind the records of USD 148 billion in 2011, USD 147 billion in 2017 and USD 135 billion in 2005.1) Hurricanes Michael and Florence in the U.S., Typhoons Jebi, Trami and Mangkhut in Asia, and Northern California’s Camp Fire were the drivers of catastrophe losses in 2018.

Despite the two consecutive years of above-average catastrophe losses, the overall rate increase fell short of the reinsurance market’s expectation. January 2019 renewals saw a meaningful price increase only for accounts with high catastrophe exposures, mostly in the U.S. and some parts of Asia. The impact of catastrophe losses on reinsurance market capacity was mitigated by alternative capital, albeit to a lesser extent compared to the previous years.

In 2018, our international treaty business achieved an 18.2 percent growth in gross written premiums, reaching KRW 567.9 billion. While the major driving force for such result was our strong performance in the U.S. and Europe, the growth was also backed by the acknowledgment of treaty statements of accounts for AY 2017 from China, which had been pending following their tax reform.

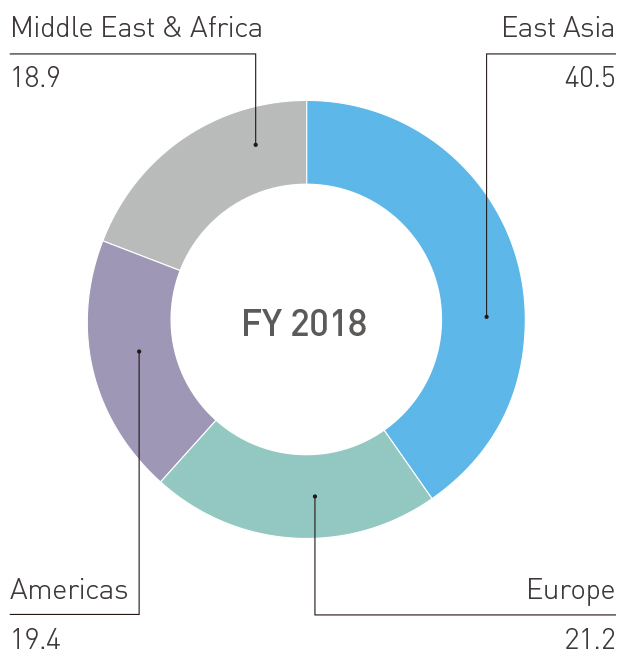

Geographically, East Asia still accounts for the largest premium volume of our international treaty portfolio at 40 percent, followed by Europe at 21 percent, and the U.S. and the Middle East at 19 percent each. Compared to the previous year, the percentage for Europe increased whereas that of the Middle East and Africa declined. This was well in line with our strategy to develop markets with higher returns.

Throughout 2019, we will endeavor to balance and diversify our book while maintaining strong underwriting discipline. Also, we will continue to focus on Europe and the U.S. for sustainable growth.

1) Weather, Climate & Catastrophe Insight 2018 Annual Report, Aon

Gross Written Premiums: International Treaty Business

(Units: KRW billion, USD million)

|

FY 2018 |

FY 2018 |

FY 2017 |

FY 2017

|

|

|

East Asia |

229.9 |

206.9 |

190.4 |

168.0 |

|

Middle East & Africa |

107.4 |

96.6 |

100.8 |

89.0 |

|

Europe |

120.6 |

108.5 |

97.7 |

86.2 |

|

Americas |

110.0 |

99.0 |

91.5 |

80.7 |

|

Total |

567.9 |

511.0 |

480.4 |

423.9 |

– Individual figures may not add up to the total shown due to rounding.

International Treaty Portfolio by Geography for 2018

(Unit: %)